Awe-Inspiring Examples Of Tips About How To Reduce Deferred Tax Liability

/TermDefinitions_DeferredTax_V1-7bcdb89b942c43268debeb7043178732.jpg)

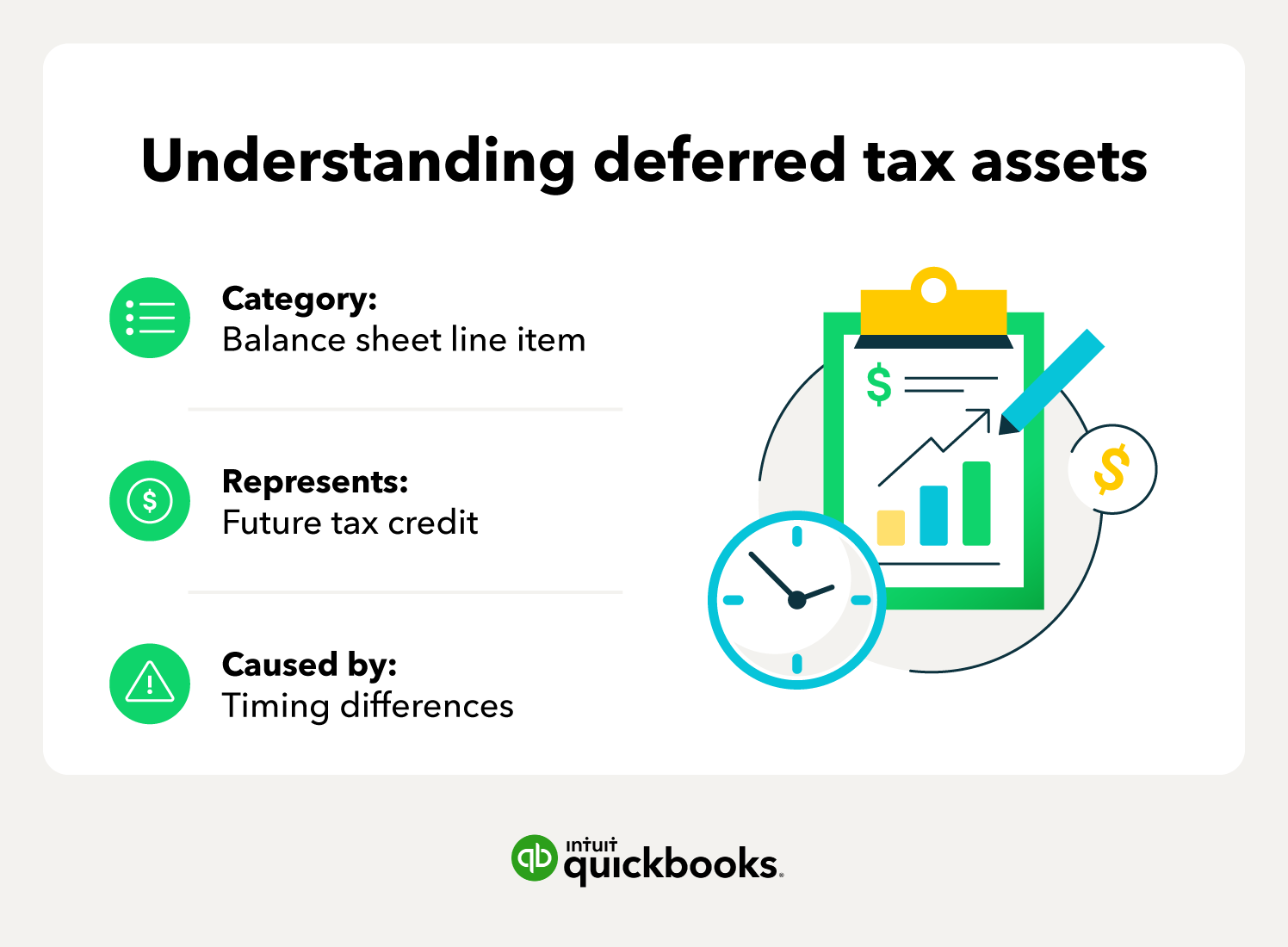

Deferred Tax Asset: What It Is And How To Calculate Use It, With Examples

Net Operating Losses & Deferred Tax Assets Tutorial

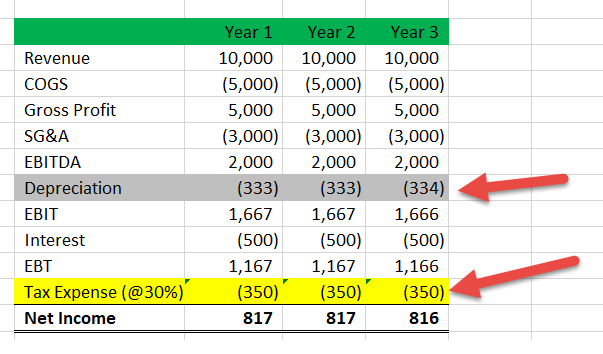

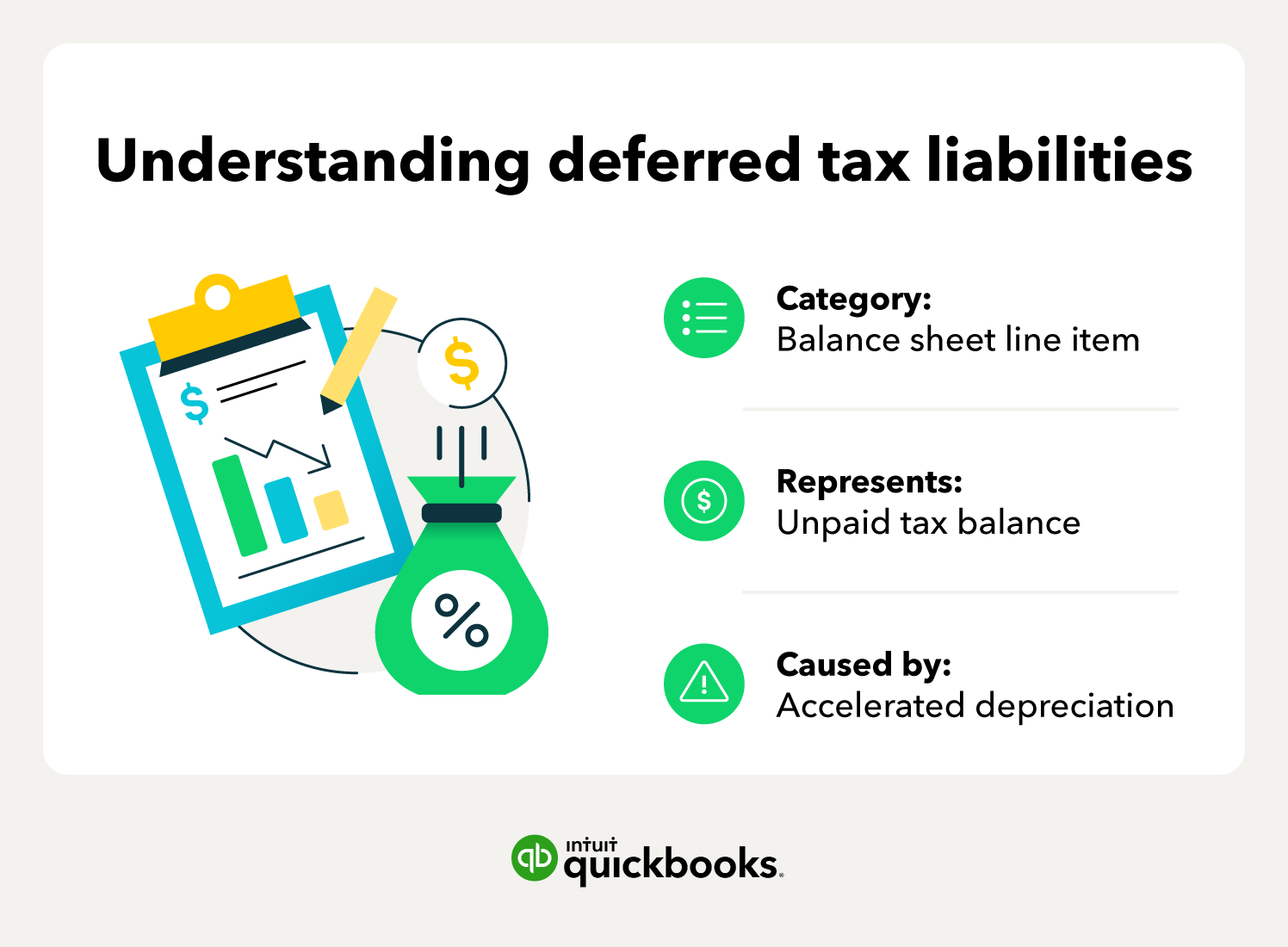

Deferred Tax Liabilities (meaning, Example) | How To Calculate?

Define Deferred Tax Liability Or Asset | Accounting Clarified

Deferred Tax - Meaning, Expense, Examples, Calculation

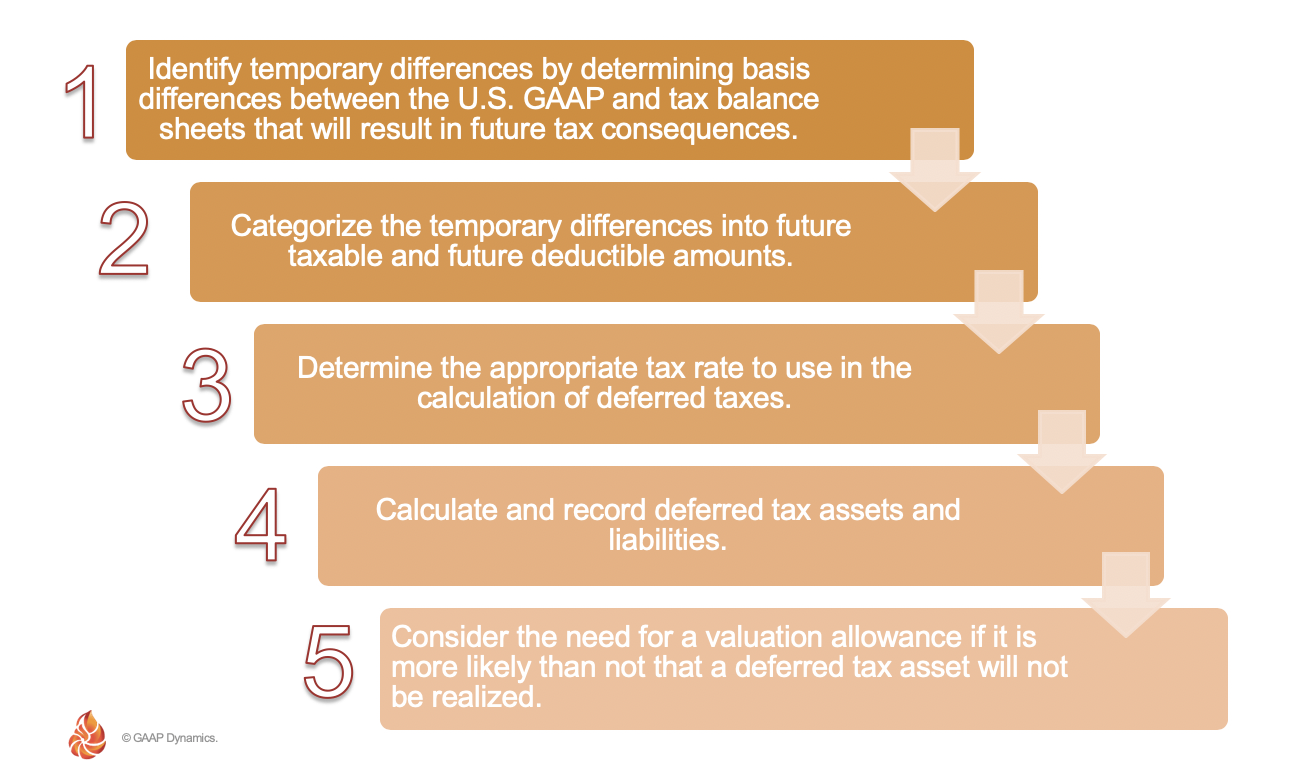

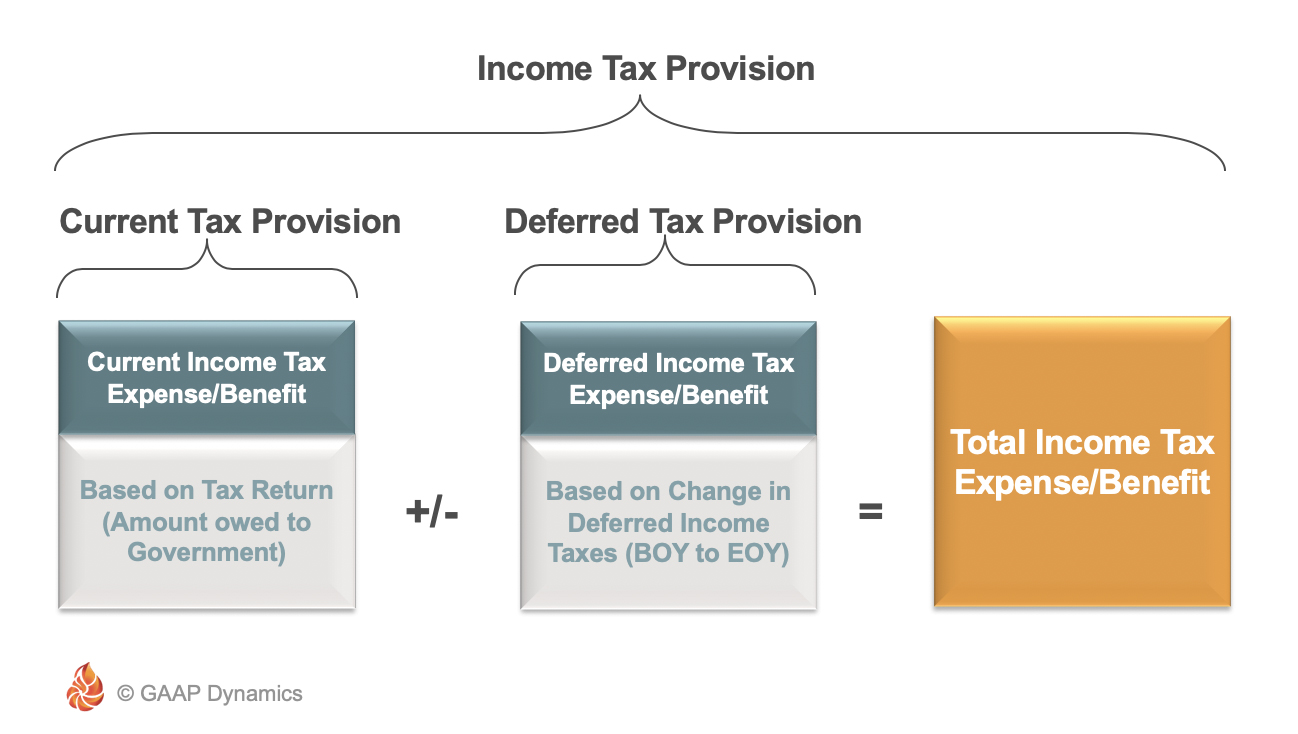

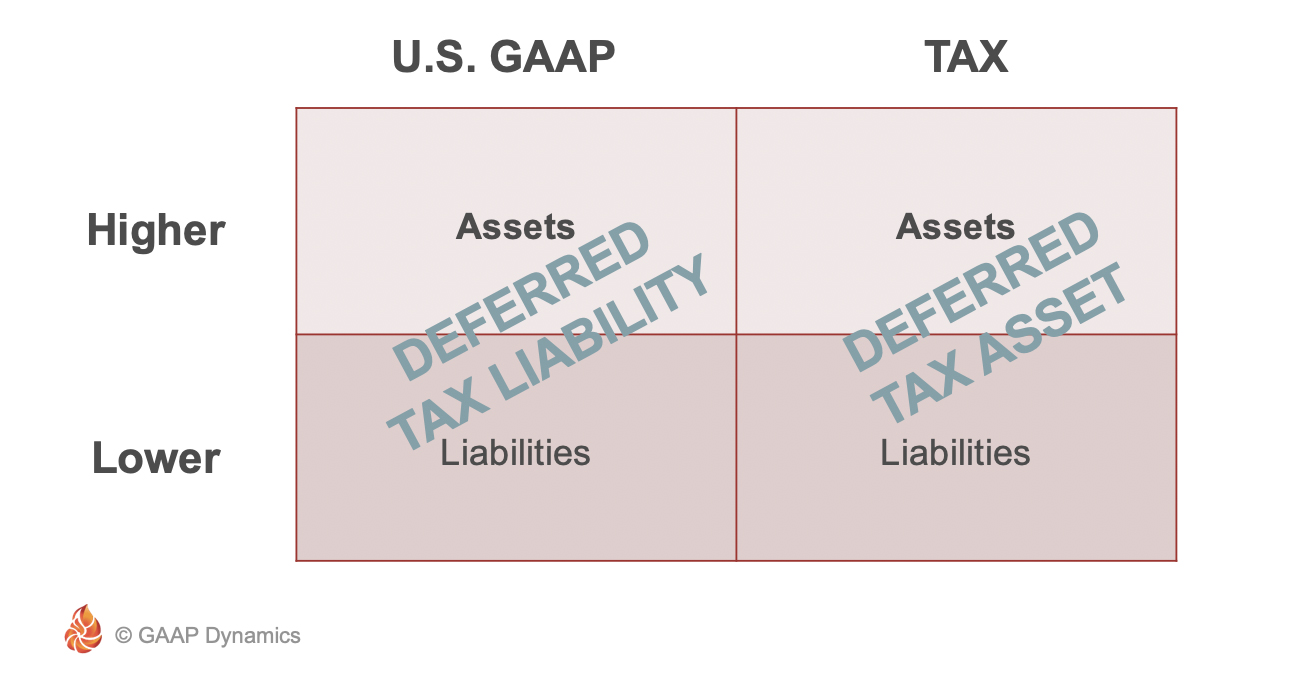

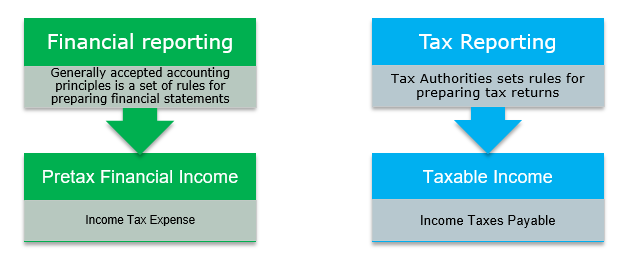

Accounting For Income Taxes Under Asc 740: Deferred | Gaap Dynamics

Valuation allowances reduce deferred tax liabilities to the amount that is more likely than not to be payable in the future.

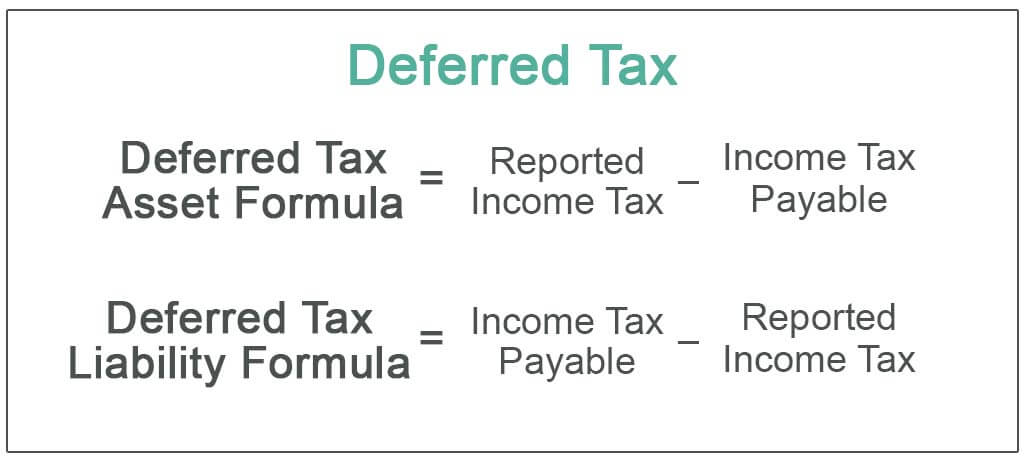

How to reduce deferred tax liability. How can a business reduce tax liability? Therefore, it cannot be based on a fair value of an asset. The measurement of deferred tax is based on the carrying amount of the assets and liabilities of an entity (ias 12.55).

In real estate, one of the most common forms of deferring tax liability is the 1031 exchange. If there is an increase in the tax rate, there would be an increase in the company’s dtl and vice versa. Changes in enacted tax rates that do not become effective in the.

With a 1031 exchange, you’re kicking the can down the road basically,. While there are numerous ways to help reduce tax liabilities (including the strategies mentioned in this article), but, it primarily involves three basic tax planning. We have a limited company client with a small profit £17,000 (the turnover is currently £1.5 million).

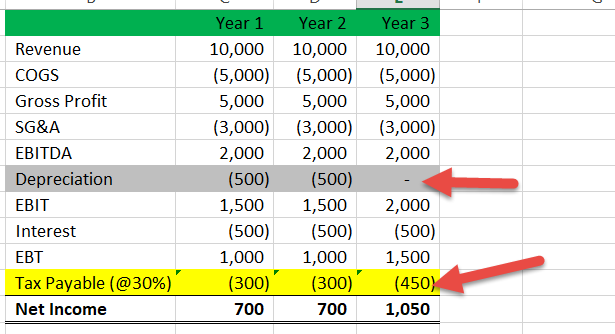

It must adjust the dtl as per the change in the tax rate. Certain tax incentives will create a deferred tax liability journal entry, giving the business some temporary tax relief, but will be collected later. Deferred tax liability is calculated by finding the difference between the company's taxable income and its account earnings before taxes, then multiplying that.

Additionally, a deferred tax asset can result from an income tax credit, loss carryover or other tax attribute that is available to reduce future income tax obligations.

Deferred Tax | Double Entry Bookkeeping

Constructing The Effective Tax Rate Reconciliation And Income Provision Disclosure

Deferred Income Tax Liabilities Explained (with Real-life Example In A 10-k)

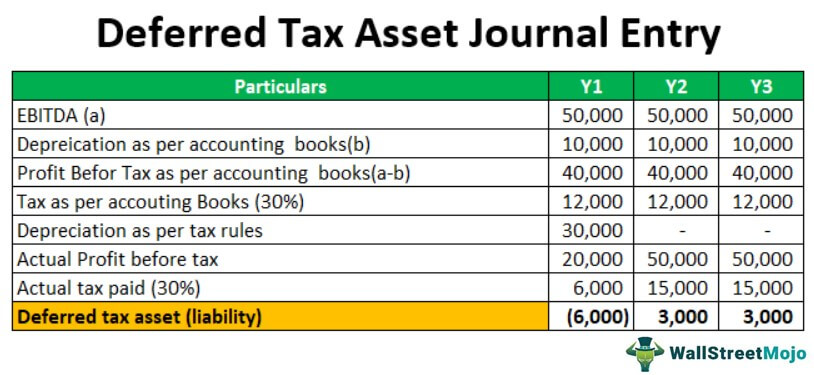

Deferred Tax Asset Journal Entry | How To Recognize?

Net Operating Losses & Deferred Tax Assets Tutorial

Deferred Tax Liabilities (meaning, Example) | How To Calculate?

What Are Deferred Tax Assets And Liabilities? - Article

Accounting For Income Taxes Under Asc 740: Deferred | Gaap Dynamics

:max_bytes(150000):strip_icc():gifv()/TermDefinitions_DeferredTax_V1-7bcdb89b942c43268debeb7043178732.jpg)

Deferred Tax Asset: What It Is And How To Calculate Use It, With Examples

Accounting For Income Taxes Under Asc 740: Deferred | Gaap Dynamics

Deferred Tax Liabilities (meaning, Example) | How To Calculate?

:max_bytes(150000):strip_icc()/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset: What It Is And How To Calculate Use It, With Examples

When A Tax Cut Is Profit Hit - Journal Of Accountancy